The interest rate in October 2025 was 4% compared with 5% at the same time last year, and the BoE has indicated a potential reduction to roughly 3.5% by late 2026.

The BoE’s August baseline forecast for UK quarterly GDP growth in Q2 2025 was 0.1%, compared with 0.2% last year, but the UK’s actual GDP grew 0.3% in Q2 2025 compared with 0.2% this time in 2024.

Against this background and along side a lack of business confidence, due to a range of factors such as the rise in NI and concerns about property related measures in the budget on 26 November, the Kent property market in 2025 has been surprisingly resilient and there has been a small degree of growth in some sectors and areas. Retail and office have performed relatively well and industrial and logistics continue to see good levels of demand and occupancy.

Science and innovation hubs continue to attract new companies and enjoy expansions. Kent Science Park has been recognised as the best life science research facility in the South East, and Discovery Park in Sandwich has doubled its scientific community, blending R&D with advanced manufacturing.

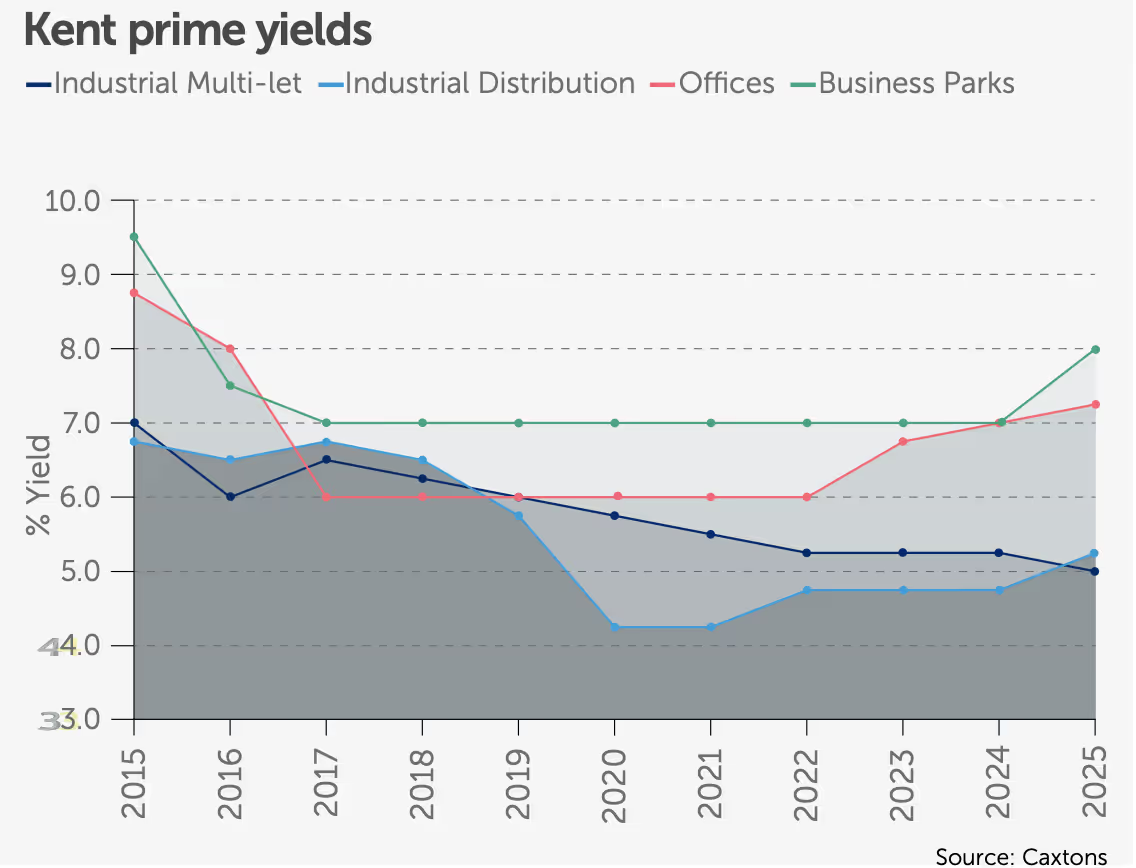

Business parks continue to attract investment in refurbishment and maintain stable yields around 8%. Praxis’s acquisition of 500,000ft2 (46,452m2) at Kings Hill signals long-term confidence, with plans for refurbishments and alternative uses. Serviced offices, particularly IWG schemes at Kings Hill and Crossways show low vacancies, while rents at Crossways have climbed to £30 per ft2, reflecting demand for quality, flexible workspace.

Hybrid working continues to shape demand, with 28% ofUK adults working flexibly. In Kent, demand is concentrated on Grade A, sustainable space, reflected in a record rent of mid £30s per ft2 achieved at One Suffolk Way in Sevenoaks. Nonetheless, take-up is sporadic, with many firms consolidating or shifting to serviced offices or spaces within their industrial/logistics buildings.

Despite this record rent, the office market has seen limited rental growth other than in Medway and Thanet, and some secondary stock is being repurposed for residential or mixed uses. South East Investment yields have held steady between 7.25% and 8.25% for prime town assets, while weaker secondary towns remain above 11.5%.

Industrial and logistics continue to perform well, underpinned by supply chain resilience, automation, sustainability and a shortage of supply in some areas. Kent hosts some of the South East’s largest ‘big box’ units, and major schemes continue to be built including at Panattoni Sittingbourne, TN2 Gateway, Tunbridge Wells, and Swanley Distribution Link. Panattoni showed its continued belief in Kent by purchasing their fourth site in Kent—70 acres (28ha) on the A20 at Lenham, in October. Demand remains strong and South East prime multi-let yields have moved in to 4.75%.

Retail continues to adapt, with food stores and retail parks leading performance. Retail sales rose by 0.5% in August 2025, building on July’s 0.6% growth. Retail parks have undergone significant reshaping. Homebase sites have been reoccupied by The Range and B&M and at Ashford’s Drovers Way retail park, long-awaited expansion is moving forward, bringing Home Bargains and a Costa Drive-Thru. Yields on retail parks have improved slightly to around 5.5—6%.

High streets show mixed fortunes. Kent towns haveseen closures, new occupiers and creative adaptations. WH Smith branches have rebranded to TG Jones, while Poundland and Costa Coffee have shut units, and Wilkos’ stores are gradually being re-occupied by a range of retailers.

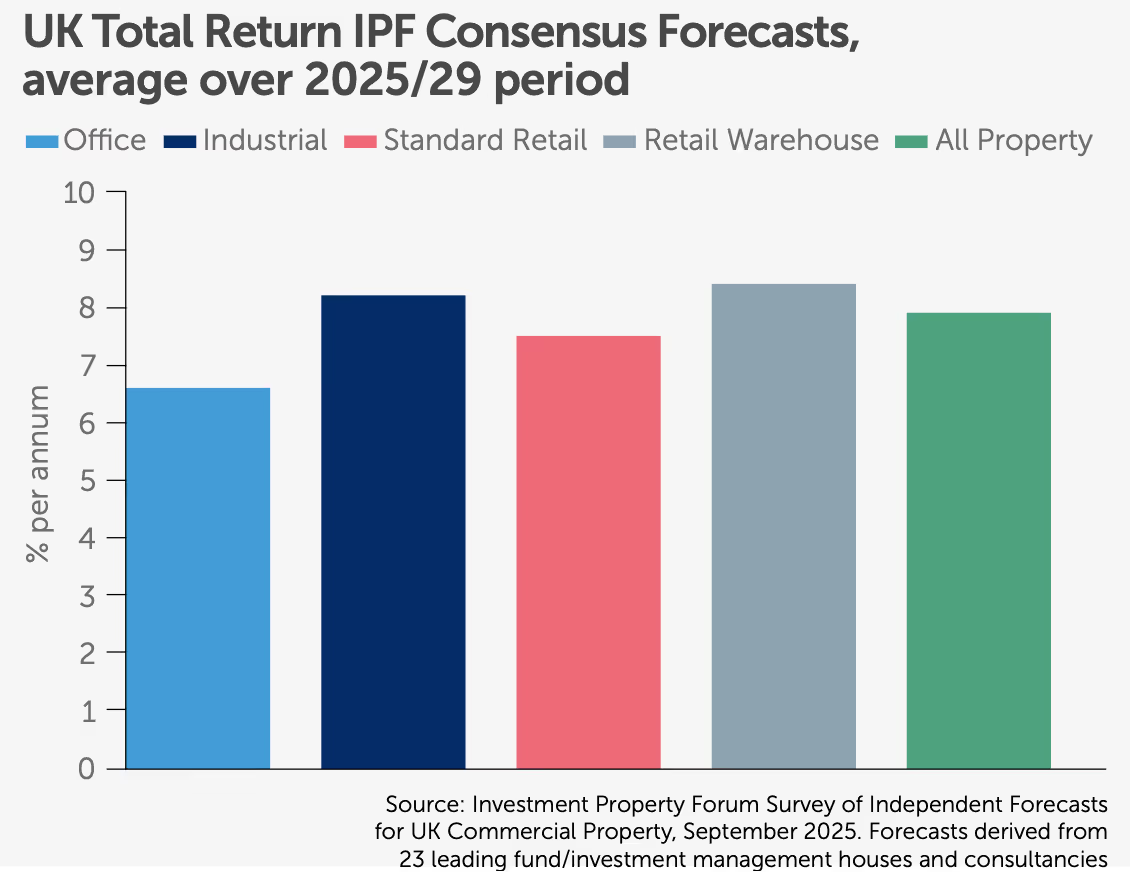

UK Total Return IPF Consensus Forecasts, average over 2024/28 period

Meanwhile, landlords are splitting units or embracing artisanal traders to sustain vibrancy. Despite pressures, towns like Canterbury and Ashford recorded rental growth of 17% and 23% respectively.

Kent’s prime retail destinations are strong with Bluewater continuing to outperform national benchmarks, welcoming Sephora, Haribo, and expanded units for JD Sports and Superdrug. Ashford Designer Outlet is celebrating 25 years, following a record-breaking 2024 with new stores such as Castore and Slim Chickens. Shopping centres present a patchwork of reinvention: Chatham’s Pentagon Centre is pivoting to health and office use, while Tunbridge Wells Borough Council is committing £68m to redevelop Royal Victoria Place with the addition of leisure-led offers.

The residential market reflects a cautious but stabilising outlook. Interest and mortgage rate reductions have boosted affordability, but cost-of-living pressures and rumours of taxes on higher-value homes temper sentiment. House prices in Kent have fallen on average by 5%, outperforming the wider South East (-7%) and England and Wales (-10%). Demand is strongest near commuter stations, with grammar schools a persistent draw for London buyers. New build sales prices per ft2 are largely down, except in Gravesham and Medway.

Nutrient neutrality challenges continue to stall development in east Kent, though mitigation credit schemes are unlocking some projects. Government reforms to the National Planning Policy Framework, including ‘grey belt’ housing, are beginning to impact approvals, as seen in Hadlow. Large projects are progressing, such as Ebbsfleet Garden City, and Westwood Village near Thanet. Demand for later living remains buoyant, with schemes advancing in Tunbridge Wells, Whitstable and in most towns.

The Investment Property Forum (IPF) consensus of independent forecasts shows a positive picture across all sectors except industrial and retail warehouse for the period 2025 to 2029 compared with 2024 to 2028. The ‘all property’ returns show a predicted 7.9% increase compared with 7.5% last year with office showing a 6.6% increase compared with a 6% increase last year, and standard retail showing an increase of 7.5% compared with 7% this year.Industrial and retail warehouse both show small decreases. This mirrors Caxtons’ findings this year, with industrial and retail warehousing’s fortunes waning slightly for the first time in many years, and office and retail doing better than for some time. However, with demand still high for industrial and warehousing, and Kent’s locational advantages for logistics, any dip in this sector’s fortunes are likely to be small.

In 2025, although some sectors have fared better than others, Kent’s property market has shown its usual resilience and appears to be cautiously optimistic, underpinned by small improvements for offices, supermarkets, retail parks, and prime retail. High streets and shopping centres remain pressured but adaptive, science parks and industrial schemes highlight innovation and growth, and the office market is being reshaped by hybrid working. Residential remains subdued but stable, with planning reforms offering hope and improvements in the medium to long-term. The regeneration section of the report in particular shows an astonishing number of projects underway in our towns and communities and this public and public/private development should encourage private investment.

Predictions are even more difficult for 2026 than usual, with the budget planned for 26 November. The Chancellor will need to raise money, that is sure, but despite the rumours and leaks, it is not clear how this will be done or how any changes might impact the property market. Nonetheless, the industry remains cautiously positive and Kent’s resilience will hopefully shine through yet again.